ESRS – European Sustainability Reporting Standards

In November 2022, we published an article about the CSRD (Corporate Sustainable Reporting Directive). A year and a half later, we’re back with a new article that complements the one on the CSRD, introducing you to the ESRS, which stands for European Sustainability Reporting Standards. This standard came into effect as of January 2024.

It’s challenging to address the topic of ESRS without mentioning the CSRD, as the CSRD indeed relies on the ESRS. The two are closely intertwined because one cannot exist without the other. To put it simply: CSRD defines the obligations of the company and the legal framework, while ESRS is the roadmap for meeting the obligations of the CSRD. The goal in creating the ESRS is to standardize sustainability reporting.

Who needs to follow this new directive? Well, all companies within the European Union subject to publishing a sustainability report according to the CSRD. The objective of both entities is the same: to submit reliable sustainability information.

The ESRD are divided into 12 categories, split into two main axes: cross-cutting standards and ESG standards.

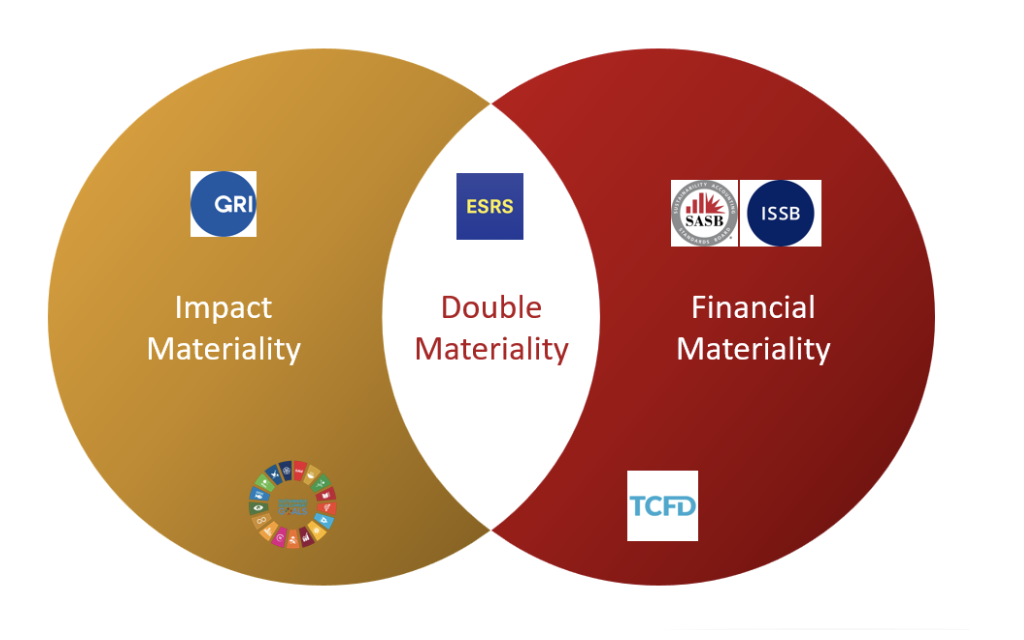

The cross-cutting standards category focuses more on general principles regarding report publication. In simple terms, it serves as a roadmap. As for the standards topics category, they are divided into 3 categories: Governance, Environment, and Social. The analysis of double materiality becomes central in the ESRS.

Key points on requirements for ESRS reports:

- Declaration of the company’s environmental, social, and economic performance.

- Identification and management of sustainability-related risks and opportunities.

- Stakeholder engagement and consultation.

- Reporting on sustainability policies, practices, and objectives.

- Compliance with international sustainability standards and regulations.

Given that this new standard is mandatory for European companies, the European Union has opted for interoperability between GRI and ISSB standards to prevent companies from having to draft a double sustainability report.

So, if you’re interested in staying at the forefront of sustainable standards, you can take our accredited course. This course will help you understand how to integrate these standards with GRI standards and learn about double materiality and how to report on the materiality assessment process. For more information about the course click here: Program